Lifting equipment rental insurance is a collection of coverage types designed to protect renters, rental companies, and third parties from financial losses arising from the possession, operation, or failure of rented cranes, hoists, slings, and rigging gear. No single policy covers every exposure in a lift.

This guide covers the core policy types required, how insurance responsibility is divided between rental companies and renters, coverage limits by project scale, how requirements shift across industries, OSHA compliance obligations, what happens when equipment fails, and how to verify insurance before a rental begins.

General liability is the baseline, but standard CGL policies exclude personal property in your care, custody, or control, which is why riggers liability and inland marine coverage are essential additions for any lifting operation.

Insurance responsibility is split between the rental company and the renter, with indemnification clauses in most rental agreements placing operational liability squarely on the renter. Understanding this division before signing is critical.

Coverage limits are not fixed. Construction projects valued between $10 million and $25 million typically require a minimum of $5 million per incident, and high-capacity equipment drives underwriters to require even higher thresholds.

Industry and job site type change the picture further. Mining operations, entertainment rigging, and large construction sites each carry distinct regulatory and underwriting requirements that standard policies may not automatically satisfy.

OSHA compliance is directly tied to insurability. Documented inspection records, load markings, and certified operator credentials are baseline evidence insurers examine when evaluating claims. Missing records can void coverage after a loss.

Renting from a full-service provider with verified inspection records and certified specialists can reduce your insurance exposure by presenting a lower risk profile to underwriters.

What Is Lifting Equipment Rental Insurance?

Lifting equipment rental insurance is a collection of coverage types designed to protect renters, rental companies, and third parties from financial losses arising out of the possession, operation, or failure of rented hoists, cranes, slings, and related rigging gear. Because standard commercial property policies often leave gaps for movable, high-value equipment, specialized coverage is essential before any lift begins.

The sections below cover the core policy types involved, who carries each, and what the coverage actually protects.

What Types of Insurance Are Required for Renting Lifting Equipment?

Several distinct insurance types are required for renting lifting equipment, each covering a different layer of risk. The following H3 sections break down general liability, inland marine, workers’ compensation, equipment breakdown, and umbrella liability coverage.

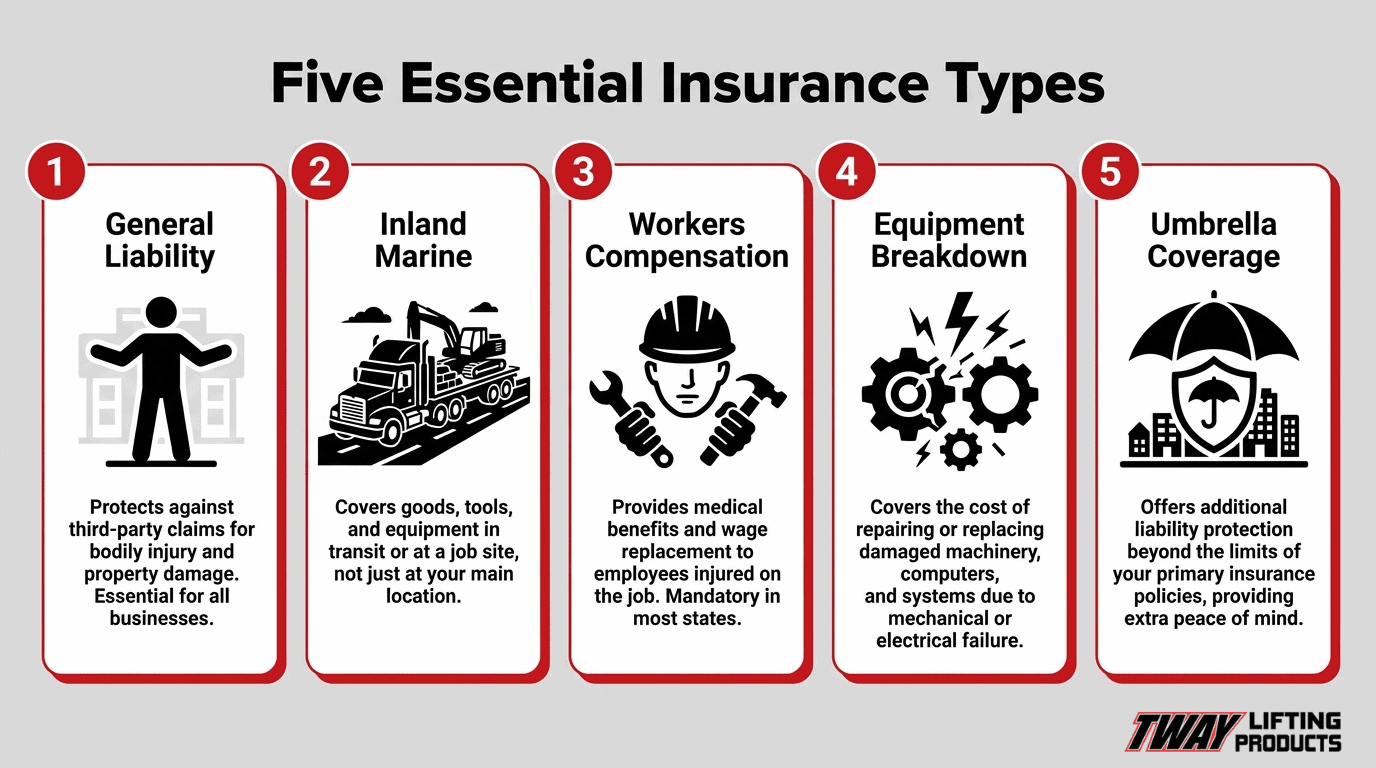

Does General Liability Insurance Cover Lifting Equipment Rentals?

General liability insurance covers lifting equipment rentals for bodily injury and property damage arising from the use of mobile equipment, per the ISO CGL coverage form. However, standard CGL policies exclude “personal property of others in your care, custody, or control,” meaning items being lifted are not automatically protected. Riggers liability insurance fills this gap directly: according to the International Risk Management Institute (IRMI), riggers liability covers a contractor’s liability arising from moving property that belongs to others, such as lifting air-conditioning units onto a roof with a crane. Many renters assume their existing commercial policy extends to rented equipment, but without specific endorsements, it typically does not. Common red flags when reviewing contractor insurance include missing general liability proof, absent workers’ compensation, or expired paperwork.

Is Inland Marine Insurance Required for Rented Lifting Equipment?

Inland marine insurance is required for rented lifting equipment when the equipment is mobile and moves between job sites, because standard commercial property policies often do not fully address movable assets. According to The Hartford, equipment rental insurance is a type of inland marine coverage specifically designed to protect equipment held for rental or lease. This makes inland marine coverage one of the most practical protections for both rental companies and renters handling high-value gear off a fixed premises.

When Is Workers’ Compensation Insurance Required During a Lift?

Workers’ compensation insurance is required during a lift whenever employees are involved in lifting operations, which carry substantial injury risk. A study published in the Journal of Occupational and Environmental Medicine found that lifting-related musculoskeletal claims accounted for 32.0% of total workers’ compensation costs in the study population. Most states mandate workers’ compensation for any employer with at least one employee, making it a legal baseline for any crew performing a lift. Crane insurance policies also typically exclude willful violations of load chart limits and inadequate ground preparation, so proper operational compliance directly supports valid claims.

Do Renters Need Equipment Breakdown Insurance for Hoists and Cranes?

Renters need equipment breakdown insurance for hoists and cranes to cover financial losses from sudden mechanical or electrical failures not caused by external events. OSHA Standard 1926.1400 governs power-operated equipment used in construction that hoists, lowers, or horizontally moves a suspended load, covering articulating cranes, crawler cranes, and mobile cranes. MSHA Standard 30 CFR 75.1400-3 additionally requires daily examination of hoists and elevators in underground mining environments. Daily insurance costs for heavy machinery like cranes can range from $150 to $500 or more depending on equipment value and risk profile, making breakdown coverage a cost-effective safeguard against unplanned downtime liability.

What Role Does Umbrella Liability Insurance Play in Rigging Rentals?

Umbrella liability insurance plays the role of excess coverage in rigging rentals, activating when a severe loss exceeds the limits of primary policies such as general liability, commercial auto liability, or employers liability. Standard general liability policies typically carry a $1 million limit, which can be insufficient when modern rigging lawsuits produce verdicts that exceed that threshold. Crane and rigging insurance programs commonly offer coverage limits ranging from $1,000,000 to $5,000,000, with higher limits available for complex construction needs. For any rigging rental involving cranes, suspended loads, or high-value property, umbrella coverage is not optional protection but a structural necessity in the insurance stack.

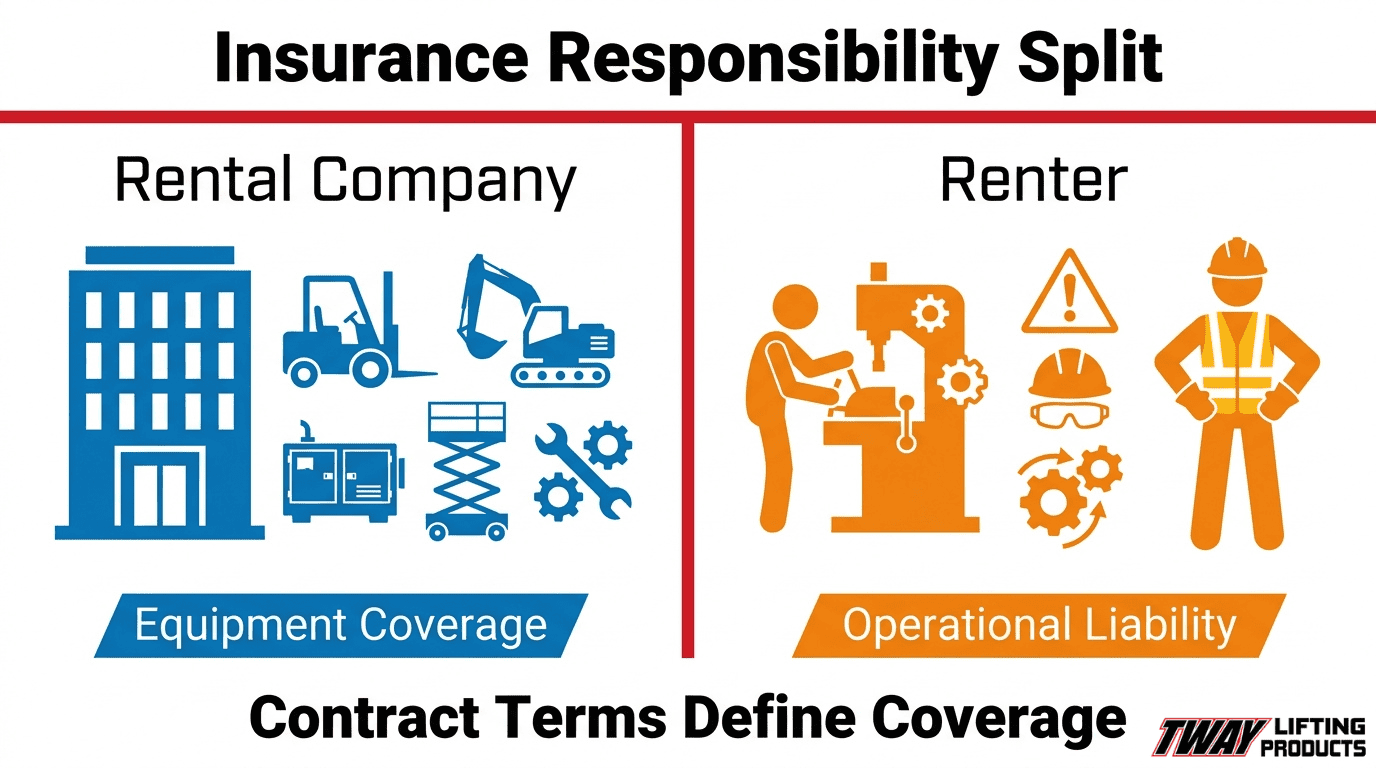

Who Is Responsible for Insurance When Renting Lifting Equipment?

Insurance responsibility in lifting equipment rentals is split between the rental company and the renter, with the rental agreement defining each party’s obligations. The following sections cover liability allocation, contract language, and whether the rental company’s policy extends to the renter on-site.

Who Carries Insurance Liability — the Rental Company or the Renter?

Insurance liability in lifting equipment rentals is carried by both parties, but the renter typically bears operational responsibility. Rental companies maintain coverage on the equipment itself, while renters are responsible for liability arising from use, operation, and site conditions.

Most rental contracts formalize this split through indemnification language. According to Law Insider’s database of equipment rental clauses, a typical indemnification clause requires the renter to indemnify and hold the owner harmless from all losses, liabilities, damages, and expenses resulting from the possession, use, or operation of the equipment. This means that if a crane drops a load due to operator error, the renter, not the rental company, absorbs the financial exposure.

What Does the Rental Agreement Say About Insurance Responsibility?

The rental agreement is the primary document governing insurance responsibility between the parties. Most agreements include three key provisions:

- Indemnification clauses shifting operational liability to the renter.

- Minimum insurance requirements specifying coverage types and limits the renter must carry.

- Additional insured endorsements requiring the rental company to be named on the renter’s policy.

Renters should review these terms before signing. Overlooking an additional insured requirement, for example, can leave the rental company unprotected and trigger contract disputes after an incident.

Does the Rental Company’s Policy Cover the Renter On-Site?

The rental company’s policy does not typically cover the renter on-site. Rental company insurance protects the equipment owner’s asset and their own liability exposure, not the renter’s operational liability. Many renters assume their commercial insurance extends to rented equipment, but without specific endorsements, that coverage often does not apply.

Renters should carry their own general liability, riggers liability, and workers’ compensation policies before taking possession of any lifting equipment. Verifying this gap before the rental begins is far more practical than discovering it after a loss.

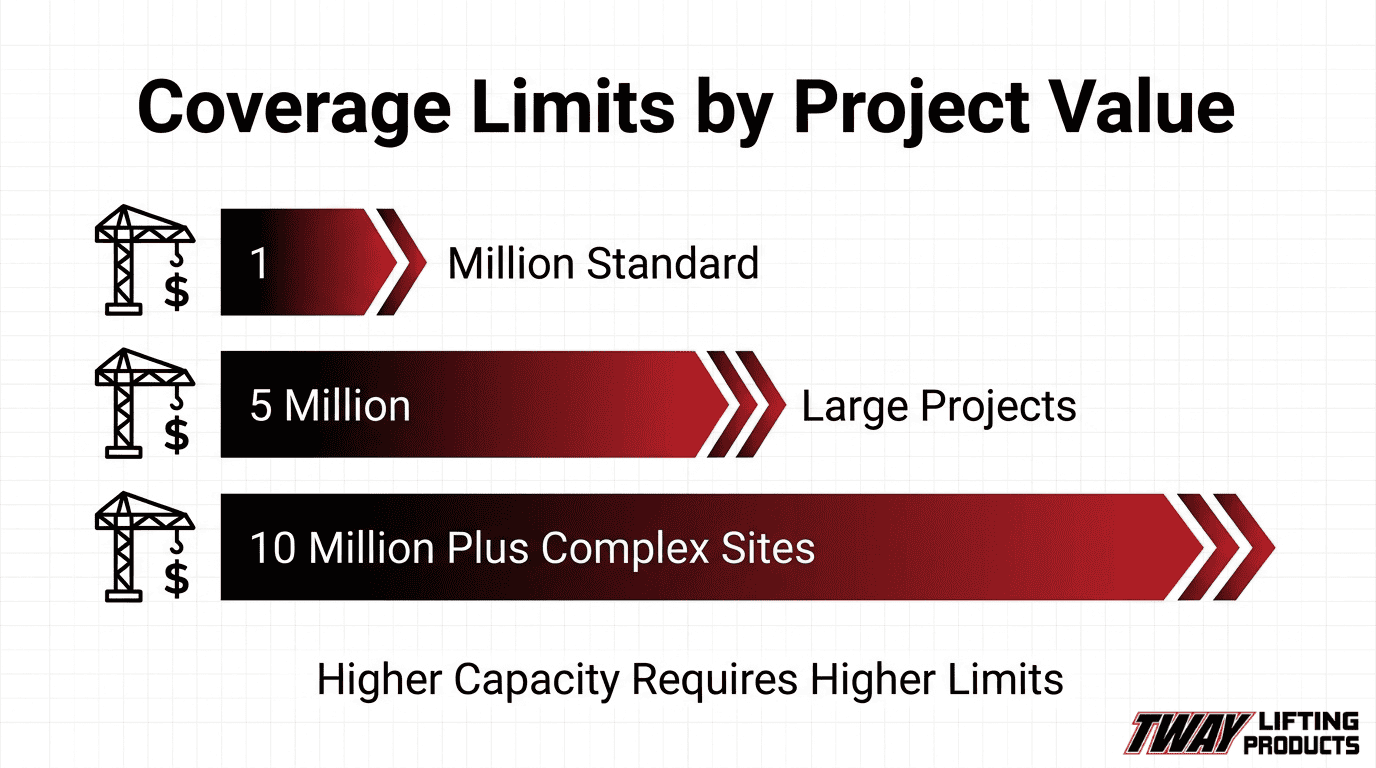

What Minimum Coverage Limits Are Typically Required for Rental Agreements?

Minimum coverage limits for rental agreements vary by equipment type, project value, and job site requirements. The following sections cover standard general liability limits, inland marine coverage for high-value lifting gear, and how lifting capacity affects requirements.

What Coverage Limits Are Standard for General Liability in Equipment Rental?

The coverage limits standard for general liability in equipment rental typically start at $1 million per occurrence. However, according to ProgramBusiness.com, this baseline is often insufficient for modern lifting operations, where verdicts in equipment-related lawsuits frequently exceed that threshold, making additional rigging liability coverage essential.

A critical gap compounds this risk: standard CGL policies exclude coverage for “personal property of others in your care, custody, or control.” This exclusion means that any customer-owned load being hoisted is not protected under a general liability policy alone. Riggers liability endorsements exist specifically to close this gap. For most commercial lifting operations, treating the $1 million baseline as a floor rather than a ceiling is the more defensible position.

How Much Inland Marine Coverage Is Needed for High-Value Lifting Gear?

Inland marine coverage requirements for high-value lifting gear are determined by the replacement cost of the equipment being rented. Spreader beams, load cells, and heavy-capacity hoists carry significant per-unit replacement values, so policies should be written to reflect actual equipment value rather than generic minimums.

Crane and rigging insurance programs commonly offer coverage limits ranging from $1,000,000 to $5,000,000, with higher limits available for specific construction applications. For high-value gear, matching the coverage limit to the equipment’s appraised replacement value is the safest benchmark.

Do Coverage Requirements Change Based on the Equipment’s Lifting Capacity?

Yes, coverage requirements do change based on the equipment’s lifting capacity. Higher-capacity equipment, such as heavy crawler cranes or large spreader beams, carries greater potential for catastrophic loss, which drives underwriters to require higher policy limits.

Rental agreements for heavy-lift equipment frequently specify minimum limits well above the standard $1 million general liability threshold. Projects with higher equipment values and greater risk exposure typically demand correspondingly higher per-incident and aggregate limits. Renters should review the rental agreement’s insurance schedule carefully, as capacity-based requirements are often non-negotiable conditions of the contract.

Do Insurance Requirements Vary by Industry or Job Site?

Yes, insurance requirements vary by industry and job site based on project scale, regulatory environment, and operational risk. The sub-sections below cover construction sites, mining and industrial applications, and entertainment rigging specifically.

What Insurance Is Required for Lifting Equipment Rentals on Construction Sites?

Insurance required for lifting equipment rentals on construction sites scales directly with project value and scope. According to the Indiana University Office of Insurance, Loss Control & Claims, construction projects valued between $10 million and $25 million typically require a minimum of $5 million per incident and a $10 million aggregate limit. Smaller sites may accept lower thresholds, but large commercial or infrastructure builds almost always demand higher limits to reflect the elevated risk exposure. General contractors frequently impose these minimums on subcontractors and equipment renters through site-specific insurance clauses in their bid packages.

Are Insurance Requirements Different for Mining or Industrial Applications?

Insurance requirements for mining and industrial applications are more stringent than standard construction coverage due to federal regulatory oversight. Mining operations fall under MSHA jurisdiction, which enforces rigorous daily inspection and certification requirements for hoisting equipment. Insurers writing policies for mining environments typically require documented compliance programs, certified operator credentials, and higher liability limits to reflect the hazard severity. Industrial facilities such as steel plants or utility infrastructure projects carry similar elevated requirements, often mandating specialized coverage endorsements that address confined-space and high-tonnage lifting exposures.

What Coverage Is Needed for Lifting Equipment Used in Entertainment Rigging?

Coverage needed for lifting equipment used in entertainment rigging includes specialized liability policies that address load failure, rigging collapse, and third-party injury in occupied venues. Per ANSI E1.47-2020, routine inspection of entertainment rigging systems is required to maintain a safe working environment and meet current industry standards. Insurers handling entertainment rigging risks typically require proof of inspection compliance, certified rigging personnel, and event-specific liability endorsements. Stadiums, arenas, and motor speedways, where Tway Lifting has direct project experience, present unique exposures because overhead rigging failures in occupied spaces carry catastrophic liability consequences.

What Does OSHA Compliance Have to Do With Lifting Equipment Insurance?

OSHA compliance directly affects lifting equipment insurance because insurers evaluate regulatory adherence when determining coverage eligibility, premium rates, and claims validity. Non-compliance creates both legal liability and coverage gaps that can leave renters and owners financially exposed.

How OSHA Violations Affect Insurance Claims for Lifting Equipment

OSHA violations affect insurance claims for lifting equipment by giving insurers grounds to deny or reduce payouts when documented non-compliance contributed to an incident. A review of 249 overhead crane incidents revealed 838 OSHA violations resulting in 133 injuries, according to OSHA Outreach Courses, demonstrating how frequently regulatory failures intersect with accident events. When an insurer investigates a claim and finds pre-existing code violations, those violations can shift or void coverage entirely. Maintaining documented compliance is not just a safety obligation; it is a critical condition of keeping your policy enforceable after a loss.

What OSHA Inspection Records Are Required to Maintain Coverage

OSHA inspection records required to maintain coverage include load markings, operator certifications, and signed inspection logs. Under OSHA 1910.179, the rated load of a crane must be plainly marked on each side, and each hoisting unit must display its rated load on the hoist or load block. MSHA 30 CFR 56.19121 further requires that the person conducting hoisting equipment inspections certify their work by signature and date, with records retained for one year. Insurers treat these documentation requirements as baseline evidence of due diligence, and missing records at the time of a claim can signal neglect, weakening your coverage position significantly.

What Happens If Rented Lifting Equipment Is Damaged or Causes an Injury?

When rented lifting equipment is damaged or causes an injury, liability typically falls on the party that controlled the equipment at the time of the incident. The sections below cover who files the claim, what standard rental insurance excludes, and when a renter’s exposure exceeds their policy limits.

Who Files the Insurance Claim When a Rented Hoist or Sling Fails?

The party who files the insurance claim when a rented hoist or sling fails depends on who bears contractual liability under the rental agreement. Most rental contracts include indemnification clauses that shift responsibility to the renter for any losses arising from possession, use, or operation of the equipment. In practice, both the rental company and the renter may file claims simultaneously, with each insurer determining coverage obligations. For large projects, the Indiana University Office of Insurance, Loss Control, and Claims notes that construction projects valued between $10 million and $25 million typically require a $5 million minimum limit per incident, illustrating how high these claims can reach.

What Costs Are Typically Not Covered by Standard Rental Insurance?

The costs typically not covered by standard rental insurance include several categories renters frequently overlook:

- Equipment in your care, custody, or control: Standard CGL policies exclude property damage to items being lifted, requiring a separate riggers liability endorsement.

- Willful overloading: Crane insurance exclusions commonly apply when operators knowingly exceed load chart limits.

- Consequential and project delay costs: Lost productivity, project downtime, and contractual penalties are rarely covered.

- Operator error without proper ground preparation: Policies may deny claims when required site preparation was skipped.

Many renters assume their existing commercial insurance covers rented equipment, but it often does not without specific endorsements.

Can a Renter Be Held Liable Beyond Their Policy Limits?

Yes, a renter can be held liable beyond their policy limits when damages from an incident exceed the coverage ceiling. Standard general liability policies typically carry a $1 million limit, which modern verdicts frequently surpass. In the Dallas crane collapse case (Mason Flores v. Bigge Crane), the contractor controlling the operator was assigned liability in an $860 million verdict, a figure that would overwhelm nearly any standard policy. Renters operating without umbrella coverage or riggers liability endorsements face the real risk of out-of-pocket exposure for the gap between the verdict and their policy ceiling. Securing umbrella liability coverage above primary layers is the most direct way to close that gap.

How Do You Verify Insurance Before Renting Lifting Equipment?

Verifying insurance before renting lifting equipment requires collecting and reviewing specific documentation from both parties. The following sections cover what a Certificate of Insurance is and what renters should examine in a rental company’s insurance paperwork.

What Is a Certificate of Insurance and Why Do Rental Companies Require It?

A Certificate of Insurance (COI) is a standardized document that summarizes an insurance policy’s key details, including coverage types, policy limits, effective dates, and the named insured. Rental companies require it because it provides immediate, verifiable proof that a renter carries adequate liability coverage before equipment leaves the facility. Without a COI on file, a rental company has no assurance that losses arising from the renter’s use of the equipment are covered. According to Hotchkiss Insurance, common red flags in contractor insurance documents include no proof of general liability insurance, missing workers’ compensation coverage, and expired or unverifiable paperwork. Requesting a current COI before any rental transaction is the single most effective step a rental company can take to screen for uninsured renters.

What Should a Renter Look for in a Rental Company’s Insurance Documentation?

A renter should look for confirmation that the rental company carries active general liability, inland marine, and riggers liability coverage with adequate policy limits. Several specific elements deserve close review:

- Policy expiration dates: Coverage must be active for the full rental period, not expired or pending renewal.

- Named insured and additional insured status: Confirm the rental company is correctly named and whether the renter can be added as an additional insured.

- Coverage types listed: General liability, inland marine equipment coverage, and riggers liability should all appear.

- Policy limits: Verify limits are sufficient for the equipment value and job scope involved.

- Exclusions language: Review for gaps, such as care, custody, and control exclusions that could shift liability unexpectedly to the renter.

Renters who skip this review often discover coverage gaps only after an incident, at which point correcting the situation becomes costly and complicated.

How Does Renting Lifting Equipment From a Full-Service Rigging Provider Affect Your Insurance Requirements?

Renting from a full-service rigging provider like Tway Lifting can meaningfully reduce your insurance burden by supplying inspected, compliant equipment with documented maintenance records. The subsections below cover how certified inspections reduce exposure and summarize the article’s key insurance takeaways.

Can OSHA-Compliant Inspections From a Certified Provider Reduce Your Insurance Exposure?

Yes, OSHA-compliant inspections from a certified provider can reduce your insurance exposure by demonstrating proactive risk management to underwriters. Insurers assess operational risk when setting premiums and coverage terms. When a provider supplies equipment with verified inspection records, documented load ratings, and certified-specialist sign-off, your organization presents a lower liability profile.

Crane and rigging insurance programs typically offer coverage limits ranging from $1,000,000 to $5,000,000, according to Risk Placement Services, with higher limits available for specific construction needs. Tway Lifting performs OSHA-required annual inspections and job site safety inspections using certified specialists, providing the documented compliance trail that insurers and project owners expect.

What Are the Key Takeaways About Insurance Requirements for Lifting Equipment Rental?

The key takeaways about insurance requirements for lifting equipment rental center on layered coverage, contractual responsibility, and verified compliance. No single policy covers every exposure in a lifting operation.

Core conclusions from this article include:

- General liability alone is insufficient: Standard CGL policies exclude personal property in your care, custody, or control, making riggers liability coverage essential.

- Renters bear primary responsibility on-site: Indemnification clauses typically transfer liability for equipment use to the renter.

- Coverage limits must match project scale: High-value construction projects often require $5 million or more per incident.

- Equipment breakdown coverage protects against mechanical and electrical failures that standard property policies do not address.

- Documented OSHA compliance directly supports insurability and can influence premium levels.

Partnering with a full-service provider like Tway Lifting, which manufactures, sells, rents, and inspects lifting equipment, simplifies compliance documentation and reduces the gaps that create costly insurance exposures.